Blockchain ? un danger pour l'industrie bancaire?par Christopher Rodriguez Université Paris Dauphine - Master 261 Banque Privée et Gestion du Patrimoine 2017 |

C. Les données personnelles : le nerf de la guerre

35

Les banques souhaitent donc décentraliser les documents KYC et pouvoir les partager via une blockchain accessible à tous les acteurs de la place, bien entendu après avoir procédé aux vérifications des documents. Cela serait synonyme d'économies, de gains de temps et de sécurité pour les établissements. En effet, Société Générale n'aurait plus besoin de récolter et vérifier les pièces justificatives fournies par Monsieur John Doe si elles ont été vérifiées par le Crédit Agricole. Nous pouvons également imaginer que chaque client dispose d'une clé individuelle, il pourrait alors choisir quelles sont les informations qu'il souhaite partager avec plusieurs établissements financiers, pour Philippe Denis « L'individu aura la main sur ses données dans un environnement distribué et il n'y aura plus de redondance des informations ». Enfin, d'un point de vue « culture client » les banques seraient gagnantes. N'avez-vous jamais dû fournir à plusieurs reprise votre pièce d'identité à votre banque ? Alors même que vous l'aviez déjà transmise quelques semaines auparavant à un autre interlocuteur ? À l'heure où les clients sont sollicités de toute part et ou les robot-advisor et autres familiy office se développent à vitesse grand V, satisfaire l'expérience client et la rendre beaucoup plus agréable doit être au coeur de toutes les préoccupations. La Blockchain pourrait donc être un allié de taille. 36 37 38 IV. Conclusion Ensemble, nous avons tenté de « décrypter » la Blockchain. Pour cela, nous nous sommes intéressés, aux fondements même de cette technologie, en analysant les principes essentiels qui la régissent. Ensuite, nous avons fait un zoom sur l'industrie bancaire, pour mieux constater comment cette technologie promettait de remettre en cause le mode de fonctionnement des banques et nous avons vu comment celles-ci se sont unies pour contrecarrer cette menace. Enfin, nous avons passé en revue de nombreuses applications concrètes, des projets sur lesquels travaillent les banques. Nous avons défini les nouvelles contraintes qui pèsent sur celles-ci, mais nous avons également vu qu'il y avait des opportunités à saisir. En somme, nous avons énoncé les conséquences pratiques pour les banques à utiliser la technologie Blockchain. Tout cela dans un but, un seul, celui de répondre à la question : « Blockchain, un danger pour l'industrie bancaire ? » De mes lectures et de mes conversations avec de nombreux experts et autres opérationnels rencontrés lors de conférence sur le sujet, il apparaît que la Blockchain a ouvert le champ des possibles et ce à plusieurs titres. Cette technologie a permis aux banques de se rapprocher via la formation de consortiums. Les objectifs de ces associations étaient multiples. Il s'agissait en premier lieu de créer des synergies communes afin de faire face à l'arrivée de nouveaux acteurs qui promettaient de mettre à mal le modèle bancaire en supprimant de nombreux intermédiaires. Dans un second temps l'objectif des consortiums était de tirer profit de ces applications en les déployant au sein de leurs structures et nous avons vu que de nombreux établissements ont d'ores et déjà pris de l'avance sur le sujet. Aussi, nous avons parlé des formidables opportunités que représente la Blockchain pour les banques à savoir : des économies de temps, économies de coût, réductions des risques réglementaires et enfin, une plus grande traçabilité des opérations laissant notament espérer à terme la mort du blanchiment d'argent. Nous avons toutefois vu que les banques et les régulateurs allaient devoir relever de nombreux défis. En effet, les questions d'ordres réglementaires, sont de nature à créer un climat d'incertitude quant à l'utilisation de la Blockchain comme moyen de preuve ou acte authentique. Régler cette question permettrait le déploiement et l'utilisation de cette technologie de manière récurrente et systématique. Nous avons soulevé la question de l'écologie et mis en exergue le côté énergivore de la Blockchain. Un autre problème de taille soulevant des questions quant à la scalabilité de la Blockchain : la vitesse 39 de transaction. Pour mémoire Blockchain valide sept transactions par seconde, là ou visa en traite quarente mille. Alors, la Blockchain va elle révolutionner la banque ? Représente-elle une menace, un danger pour l'industrie Bancaire ? Il est selon moi trop tôt pour apporter une réponse catégorique sur le sujet. Tout est une question de patience, ce qui manque parfois au monde de la finance. L'Histoire nous l'a souvent montré, prenons par exemple les évènements de 2001 et la fameuse crise de la bulle internet, les banques et les marchés financiers peuvent surestimer les impacts des nouvelles technologies à court terme, et paradoxalement les sous-estimer à long terme. Cette fois, les banques ont été forcés de réagir rapidement en déployant des stratégies à court et moyen terme pour faire face à l'arrivée de nouveaux concurrents. En définitive, la Blockchain risque bel et bien de faire évoluer le modèle bancaire. Peut-être assisterons nous à la disparition de certains acteurs ou certains métiers, mais il se pourrait également que la Blockchain fasse émerger de nouveaux standards ou de nouvelles règles qui seront alors profitable à l'économie en générale, mais aussi et surtout au plus grand trésor des banque : les clients. 40 41

V. Annexes Description du post-marché : Christopher Rodriguez- Paris Dauphine A) Le métier titres La conservation Le métier de conservateur est appelé « custodian » en Anglais. C'est une activité qui consiste à gérer toutes les opérations post-marché liées aux portefeuilles de titres des investisseurs du marché. Le custodian s'occupe d'assurer la tenue des comptes ainsi que la conservation des avoirs ou titres de ses clients. Son rôle est donc d'enregistrer toutes les opérations d'achats/ventes et de souscriptions/rachats, d'en assurer le règlement ainsi que la livraison. Mais ce n'est pas tout, il se charge de tenir à jour les comptes titres et traite les diverses opérations sur titres telles que les paiements de dividendes, les souscriptions-rachats ou encore les offres publiques d'achat. En résumé, le conservateur joue aujourd'hui le rôle de coffre-fort. Ce coffre est loué à des clients pour que ceux-ci puissent y déposer leurs titres, ou autres créances. La seule différence réside simplement dans le fait qu'aujourd'hui, les titres ne sont plus physiques (papier), mais totalement dématérialisés. La fonction dépositaire Le métier de dépositaire appelé « depositary »ou « trustee » en anglais. Son rôle est de veiller sur l'ensemble des actifs appartenant aux fonds d'investissement (Organisme de Placement Collectif). Parmi ces actifs, nous retrouvons bien entendu les titres, les espèces, les produits dérivés, mais aussi les opérations de gré à gré. À ce titre, le dépositaire est donc généralement aussi le conservateur. Le dépositaire doit veiller à la conformité des caractéristiques qui ont été déposées auprès de l'Autorité des Marchés Financier, nous pouvons parler du prospectus du fond. Il s'assure par exemple de la répartition des investissements. Si le fond d'investissement déclare investir 40% des actifs en France, le dépositaire doit s'assurer que soit bien le cas. Il travaille donc en étroite collaboration avec son client et l'alerte sur toute anomalie ou potentiel sujet litigieux. En revanche, il ne peut informer son client si des enquêtes sont diligentées par l'autorité des marchés financiers. 42 La centralisation ou tenue de registre 43 Le dépositaire peut également se voir confier la gestion du passif du fond. Il joue donc également un rôle de centralisateur et gère la transmission ainsi que le règlement-livraison des souscriptions-rachats de parts. Arrêtons-nous un instant sur ce rôle de centralisateur. Le centralisateur comme son nom l'indique s'occupe de centraliser tous les ordres de souscription, mais aussi de rachats de parts émanant des investisseurs. Le centralisateur est donc en liaison quasi-permanente avec le gérant du fond à qui il transmet ses informations concernant les souscriptions-rachats selon une périodicité défini en amont. Avec ces informations, les gérants de fonds vont savoir s'ils vont pouvoir disposer de cash supplémentaires dûs à un nombre de souscriptions supérieures aux rachats. Si c'est le cas, alors ils vont pouvoir investir ce cash selon les caractéristiques qui ont été transmises à l'AMF et communiquer aux clients lors de leur investissement. En revanche, si la situation inverse se produit et qu'un excès de rachat se présente les gérants vont devoir faire des versements aux porteurs pour ce faire, ils vont être contraints de liquider une partie des lignes du fond. Ainsi, nous comprenons aisément que le centralisateur doit être capable à tous moment de communiquer sur le nombre de parts de l'OPCVM qui sont en circulation. Cet élément important entre dans le calcul de la valeur liquidative du fond (la valeur de la part) qui est égale à l'actif net du fonds divisé par le nombre de parts. Distinguo : dépositaire local, dépositaire global, sous dépositaire et dépositaire central de titres Afin d'être précis dans ma description du métier titre, il convient selon moi de faire un aparté sur la chaîne post-marché et plus précisément de faire un zoom sur les rôles des dépositaires et ceux des dépositaires centraux. Le post-marché concerne tout les instruments financiers à savoir les titres, actions, obligations, OPCVM, dérivés, etc. C'est la vie du titre après son achat (passage vers la contrepartie et gestion du titre par le dépositaire central.) Le dépositaire central Certains noms de Dépositaires centraux ne vous sont pas inconnus. L'un d'entre eux plus particulièrement puisque son nom a été rendu célèbre en Fevrier 2001. Après s'être trouvé au centre d'un gigantesque scandale judiciaire sans précédent. Vous l'aurez deviné, il s'agit bien évidemment de Clearstream qui est présent en Allemagne et au Luxembourg. Vous avez également sans doute entendu parler d'Euroclear, qui est présent en France, 44 en Belgique, aux Pays-Bas, au Portugal, en Suède, en Finlande ou encore au Royaume-Uni et en Irlande. En revanche, ce que vous ignorez sans doute, c'est le rôle de ces organismes. Ce qu'il faut avoir en tête, c'est que le dépositaire central est responsable de la tenue du compte émetteur lors de chaque émission d'actions, obligations ou titres de créance négociables. Il est donc dans l'obligation de veiller à ce que le montant total des quantités en possession des intermédiaires (banque, compagnie d'assurances) soit égal aux quantités émises par les différents émetteurs. Alors pour que toutes transactions soient validées et donc dénouées, un transfert doit être fait sur les livres du dépositaire central. Il est important de préciser que le dépositaire central ne connaît pas le nom des porteurs des titres qui ont été déposés sur les comptes ouverts par les intermédiaires et les banques. Exemple : Nous avons la société de gestion Amundi qui dépose 450 titres de la société Orange et Swiss Life qui en déposent 300 en Italie chez le même intermédiaire appelé Local Custodian (Société Générale Securities Services par exemple) puisque nous sommes à l'étranger. Et bien le dépositaire central n'est pas en mesure d'identifier séparément et nominativement les propriétaires de ces titres. Les réglementations nationales et autres directives (UCITS V ou en encore AIFM dont nous parlerons plus tard) commencent tout juste à obliger les conservateurs / local custodian à faire inscrire leurs avoirs propres sur un compte dédié, de sorte qu'ils ne soient pas mélangés avec les avoirs que possèdent leurs clients. Cette technique est appelée ségrégation des actifs. Cette ségrégation des actifs a pour mission de protéger les intérêts des investisseurs particuliers ou professionnels des tirages sur la masse qui est une pratique totalement interdite. Cette expression désigne une pratique passée ou le dépositaire local utilisait à l'insu de ses clients les titres pour reconstituer sa trésorerie ou pour garantir des opérations de type monétaire. Ils étaient donc sans le savoir exposé à un risque de crédit provenant de la contrepartie des intermédiaires à qui ils avaient confié leur avoir. Pour finir tout dépositaire central procède au règlement-livraison. Celui-ci reçoit diverses instructions. Soit il reçoit des titres, soit il a pour instruction de livrer des titres. Ces opérations ont toutes vocations à déclencher des mouvements d'espèces ou de titres sur les comptes de ses clients. Le traitement des flux financiers étant une absolue nécessité, les dépositaires centraux doivent avoir soit le statut de banque (c'est le cas de Clearstream), soit utilisé des systèmes de transfert automatique de cash (Target 2) qui permet de transférer de gros montant par-delà les frontières. Dépositaire local, global et sous-dépositaire Faire appel à un dépositaire est indispensable pour accéder directement à un marché local ciblé. L'inconvénient pour les investisseurs est que pour chaque nouvelle devise, chaque nouveau marché, il faut impérativement faire appel à un nouveau prestataire par le biais d'appels d'offres par exemple. Toutefois, cette démarche étant trop fastidieuse bon nombre d'Institutionnelles ou de Grandes Entreprises désireuses d'intervenir sur tel ou tel nouveau marché financier vont vouloir nommer un seul et unique intermédiaire... Le dépositaire global. C'est chez le dépositaire global que vont être déposé les avoirs financiers et les titres, c'est donc à lui que revient la mission de rentrer en contact avec les intervenants des marchés locaux, et ce, en faisant appel à ses sous-conservateurs qui sont en réalité des conservateurs locaux. Ils se chargeront donc d'exécuter pour le compte du dépositaire global les transactions de ses clients (Institutionnelles ou Grandes Entreprises). Les sous-conservateurs sont donc en charge d'assurer la gestion des avoirs qui sont détenus sur les places financières étrangères par l'investisseur. Chacun d'entre eux adhère au système de dépôt et de règlement-livraison de son propre pays. Il est également chargé d'entretenir les relations avec les autorités de références... L'investisseur confie au dépositaire global toutes opérations aux différents acteurs financiers de sa propre place. Vous l'avez compris le conservateur global ne décide pas et ne négocie en aucun cas à la place de son client. Il n'est intervenant après la négociation et c'est grâce à son réseau de sous-conservateurs que le global custodian va pouvoir avoir accès à de nombreuses places de marchés situées aux quatre coins du globe. Peu importe le nombre de sous-conservateurs le client lui n'aura donc qu'un seul interlocuteur en ce qui concerne le post-marché... Le dépositaire global. 45 L'administration de fond 46 Finissons avec une activité que peut exercer également le dépositaire. Il s'agit de l'administration de fond. Cette activité a pour mission de prendre en compte l'ensemble des opérations d'investissement réalisées sur le fond de manière à retranscrire comptablement de manière la plus fidèle les opérations enregistrées par le front office. Pour effectuer la valorisation des portefeuilles de ses clients, le dépositaire doit donc calculer la valeur de la part de chaque fonds qui lui sont confiés. La valorisation de l'actif dépend de la valeur liquidative comme nous l'avons très brièvement vue précédemment. La valeur de la part est égale à l'actif net du fonds divisé par le nombre de part total. C'est cette valorisation des actifs permettra d'établir les comptes de l'OPC. Le plan comptable des Organisme de Placement Collectif doit respecter les principes du Plan Comptable Général. Il est, en revanche, spécifique aux OPC et défini donc des règles spéciales. Tout acte de gestion qui impacte le patrimoine de l'OPC doit impérativement être mentionné dans les comptes annuels. Ces comptes seront ensuite validés par un commissaire aux comptes. Un des principes fondamentaux de ce code est le principe de prudence et d'égalité aux regards des porteurs. L'ensemble des règles qui permettront l'évaluation des actifs composant le fond doivent impérativement apparaitre dans le prospectus transmis à l'AMF et au client. Depuis 2003, il est obligatoire de valoriser les actifs à leur valeur actuelle. Elle est définie par la valeur de marché si la valeur liquidative est calculée de manière quotidienne, hebdomadaire ou mensuelle. Si ce n'est pas le cas (private equity par exemple) l'évaluation se fera par modèle financier. La valeur liquidative tient compte de la vie du fond et intègre l'ensemble des informations à savoir les détachements de coupon, le paiement des dividendes, etc. C'est la raison pour laquelle les sociétés de gestion sont en contact permanent avec leur dépositaire et leur valorisateur qui vous l'avez compris peuvent être la même entité. 47 The blockchain folk theorem* Bruno Biaist Christophe Bisiöret Matthieu Bouvard S Catherine Casamattafl May 22, 2017 Preliminary Abstract Blockchains are distributed ledgers, operated within peer-to-peer networks. If reliable and stable, they could offer a new, cost effective, way to record transactions and asset ownership, but are they? We model the blockchain as a stochastic game and analyse the equilibrium strategies of rational, strategic miners. We show that mining the longest chain is a Markov perfect equilibrium, without forking on the equilibrium path, in line with the seminal vision of Nakamoto (2008). We also clarify, however, that the blockchain game is a coordination game, which opens the scope for multiple equilibria. We show there exist equilibria with forks, leading to orphaned blocks and also possibly to persistent divergence between different chains. *We thank B. Gobillard, C. Harvey, J. Hoerner, A. Kirilenko, T. Mariotti, S. Villeneuve, the members of the TSE Blockchain working group, participants in the Inquire Conference in Liverpool, 2017, as well as an anonymous referee for helpful comments. Financial support from the FBF-IDEI Chair on Investment banking and financial markets value chain is gratefully acknowledged. This research also benefited from the support of the Europlace Institute of Finance. t Toulouse School of Economics, CNRS (CRM-IAE) t Toulouse School of Economics, Université Toulouse Capitole (CRM-IAE) S Desautels Faculty of Management, McGill University 1 Toulouse School of Economics, Université Toulouse Capitole (CRM-IAE) 1 6. Nodes express their acceptance of the block by working on creating the next block in the chain, using the hash of the accepted block as the previous hash.' The nodes conducting the above mentioned tasks arc called "miners", as they "mine" to solve proof-of-work problems, 53 and get, rewarded for this in bitcoins. When mining, a miner sets a 53 The problem to be solved by the miners is a purely numerical problem, completely unrelated to the economic nature of the transactions in the block. Once found, the solution to this problem is easy to verify. computer capacity that performs trials to find a hash value lower than a given threshold. Each trial is independent: past failures do not affect thc probability of success of a future trial. Once a trial is successful, the winning miner sends the block with the solution to other participants. If participants accept, this block as the new consensus, they take it as the parent of the new block they start mining. In that case (unless the consensus is altered), the miner who solved the block gets a reward. 4 This process is illustrated in Figure 1.

48 Figure l: The Blockchain At t 0, there is an initial block Bo and a stock of transactions included in a block 131, chained to BC). Miners work on a cryptographic problem until a miner solves Bl at [l . Bl is broaclcast to all. Nodes check proof-ofi work and transactions validity, and express acceptance by chaining the next block to Bl. Ideally, there is only onc chain, to which all miners attach their blocks. One of the major questions about, blockchain is whether such an outcome will arise. The alternative outcome is onc in which miners do not, all attach their block to the same chain. Suppose, e.g., that the last, block solved is Bn, but miner m chains his next block to the parent, block of Bn, i.e., Bn 1. This starts a fork, illustrated in Figure 2. If some miners follow m, 3 throughput. 54 Two main solutions, Segregated Wit,ncss (SegWit) and Bit,coin Unlimited (BU), are supported by different, Bitcoin community members, with the threat of some to fork in an attempt to impose their preferred solution. As of May 2017, it, is not, clear which solution will be adopted, nor whether it will lead to a fork. How do forks happen? The above coordination issues, which can arise following a technological change or an unpredictable event; (like the hacking of TheDAO) have been overlooked and it is a contribution of the present, paper to undescorc and analyse them. Coming from a different, angle, an often mentioned potential cause of forks is "double-spending." Suppose miner m from the example above buys an object from some party Y a,nd the transfer of m's bitcoins to Y is recorded in B,. This could give an incentive for miner m [o mine from Bn,-l, trying [o attract miners to his chain, to orphan Bn and void the transfer of his bit,coins to Y. m would then be able to spend his biccoins again, i.e., would "double spencl.' 'I This includes rewards given by the blockchain system plus transaction fees which the originators of trade can choose to offer for the valida,tion of their transactions. 54 Precisely, the protocol sets the maximum size of a, block of transactions to one megabyte, which slows down the speed of transactions validation and hinders the development of the network itself. 49 Non-instantaneous dissemination of information through the network is another potential reason why forks, i.e., competing versions of the ledger, could arise. Na,kamoto (2008) identified that problem and suggested it would be solved if miners always chained their blocks to the longest, chain: "Nodes always consider the longest chain to bc [he correct one and will keep working on extending it. If two nodes broadcast, different versions of the next, block some nodes may receive one or the other first. In that, case, they work on the first one they received, but, save t,hc other branch in case it, becomes longer. The tie will be broken when the next, proof-ofwork is found and one branch becomes longer; the nodes that, were working on the other branch will then switch to the longer one.' In the present paper, we abstract from these two problems, assuming miners do not, attempt to double spend and also that, information is instan disseminated in

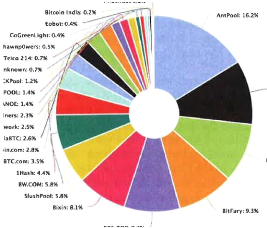

the network. In this 5 sufficiently many blocks have been attached to that chain (this is the socalled " k-blocks rule"). This can lead miners working on different chains to continue to do so, in order to beat the competing chain. This can contribute to the emergence of persistent forks (Proposition 3). While the persistent forks result hinges on the strategic behaviour of miners, who anticipate their strategy will affect the value of their rewards, the emergence of forks, making the previously longest chain orphan, relies only on coordination effects, and would also arise in a competitive environment. In the last section of the current paper, we discuss how integrating frictions in our model, such as attempts to double-spend or non-instantaneous dissemination of information, could provide further insights into the blockchain 's stability. We also suggest to endogenise the computing capacity that each miner installs on the network. In the Bitcoin protocol, total computing capacity determines the difficulty to solve blocks. Because each miner does not take into account the impact of his computing capacity on the diffculty of the cryptographic problem faced by other miners, we conjecture that an arms race can occur, leading to over-investment in computing power (not unlike the over-investment in financial expertise noted by Glode, Green and Lowery (2012)). This provides a roadmap for our future research. Literature: Most existing literature on blockchains is in computer science, with the notable exceptions of Harvey (2016), who discusses the pros and cons of blockchains and Yermack (2017) who discusses their implications for corporate governance. 50 Computer science papers offer insightful analyses of potential strategic problems, but usually do not rely on the same type of formalism as in economics. Bonneau et al. (2016) analyse how mining pools (i.e., groups of miners) controlling a large fraction of the computing power could attack the chain. Eyal and Sirer (2014) show how colluding miners can obtain a larger revenue than their fair shares. Teusch, Jain and Saxena (2016) study how a strategic miner can fork and attack the blockchain to double spend. The paper to which our analysis is the closest is Kroll, Davey and Felten (2013). They note that the interaction between miners should be analysed as a game. They argue that the LCR is a Nash equilibrium. While their analysis offers interesting economic intuition, it does not offer a formal analysis and proof of equilibrium. Another difference between our analysis and theirs is our analysis of forks on the equilibrium path. 7 Thus, a reasonable order of magnitude for IVI is around 15. Because the number of pools is finite, it PHash.lO: 0.2% F2Pool: 10.6% 8TCC Pool: 9.7% is appropriate to take a ga,mc approach, in which each of the M

players behaves

shawnpOwers: Unknown: Kano CKPool: BATPOOL: CANOE GBMiners: BitClub Network: ViaHTC: BTC.TOP: 9.2% Figurc 3: Hashrate distribution of Bitcoin mining pools on April 20, 2017. Source: blockchain.info. servers are located in China. The other three main pools have servers in China, .Japan and the US. Mining technology: There is a continuous flow of transactions sent for confirmation by end-users. 6 For the moment, for simplicity, we assume all miners perfectly and instantaneously observe this flow, which they include in the blocks they mine. The time it takes a miner to solve his block depends on the difficulty of the cryptographic problem and the miner's computing 51 fiFor simplicity we, take the flow of transactions to be exogenous, while in practice it can a,ctually be endogenous. hi fact, we don't model the transactions and model the blockchain process directly at, the level of the blocks. 9 economic mechanisrn we analyse below. Wc assume that at time exponentially distributed, with parameter Awn, , miner m is hit by a liquidity shock. At time the miner must, leave the game and sell the cryptocurrcncics hc earned previously to a new miner who also inherits his beliefs and preferences. 55 Thus, exits are compensated by ent,ries and the environment is stationary. Blockchain: At time 0, there is an initial state of the ledger, encoded in 130, and a set, of tra,nsactions. Starting from 130, miners start working on the first block, 131 , which contains the initial set, of transactions. Once Bl is solved, miners must choose t,o which parent, block to chain the next, block (132) they mine. If minors choose B] as a parent block, they continue the first, chain. Alternatively, miners ca,n choose to disregard B] and attach B2 to BC). In that case, miners start, a fork and there are two competing chains, one including 130 and B], the other Bo and B2. As the, game unfolds, a tree of blocks develops. In the above example, once B2 is solved, the tree has three vertices: 130, Bl and 132. If miners continue the first chain, by attaching B2 to Bl the two edges (or branches) of the tree are (Bo, Bl) and (131 , 132). In contrast, if miners start, a fork, the two edges arc (130, B]) and (Bo, 132). At, each vertex 13k, the tree also includes a label, identifying the miner who solved the corresponding block, The indices of the blocks give the order in which they have been solved. That is, if k < n, then block 13k was solved before block Bn. In general, at, any time l, one can observe a tree of solved blocks C t {P}, E l', I l'}, where B t (130, ...Bn,) is the set, of all blocks that have been solved by time t, E l {(B(), DI), ...Wk, Bw), ...1, with < k: < k' < n, is the set, of edges chaining t,hcsc blocks, and I L = ...m(Bn)) is the set of identities of miners who solved blocks. Within a tree, a chain is a sequence of connected blocks in which each block is connected to at most, one subsequent, block. Thus, cach fork starts a new chain. More formally, we define a fork as follows: Definition 1 Fork;: Th,cre is a fork: at time t 'if a,nd only i/ there exists (Bi, Bk, Bkl) 'included 'in B t such that (Bi, 13k) a,nd (Bi, 13k,) belong to E l . It, is also useful to define the original cha,in for a given tree C", as follows: 11 practice, miners do not sell their reward immediately after they have earned it. In particular, the so called " k-blocks rule" implies that the cryptocurrency obta,incd by m for solving a block will be, accepted by others only after sufficiently many blocks have been chained to that, block. At time the, payoff from each solved block depends on the credibility of the cha,in that, contains the block. Consider two polar cases: In the first case, a block solved by a mincr becomes orphaned, i.e., no further blocks are att,ached to it, so that, no miner expresses acceptance of that block and 55 Wc explain below the process through which miner m accumulates crypt,ocurrcncies. 52 the transfer of crypt,ocurrcncy it, encodes. In the second case there is a single chain to which all blocks belong, reflecting consensus on the blocks in that, chain. The value of a rewa,rd in the first case, is likely to be zero, and is bound to be smaller than in the second case. Next, consider an intermediate case, in which the block is included in a chain competing with another one. As long as a significant fraction of the miners are working on each of the chains, the value of rewards included in the blocks of the two chains, while uncertain, can remain positive. More formally, we assume (hat (he payoff for miner m, from solving B is an increasing function, G(.), of the number of miners active at time zm, in the chain including B. For exa,mple, suppose there, are two act,ivc chains at time zm,. If [herc arc K miners active in the chain including B, and M -- K in the other, the payoffs from solving blocks are the following: The miner who solved block B, which we denote by m,(B), earns G(K) for block B. A miner who solved a block in the other chain earns G(M -- K) for that block. If a miner solved a block that, belongs to both chains, he earns G(M -- K) + Wc assume that, G(O) G(l) = since, when there is only onc or no miner on a chain, the associated cryptocurrency has no value. Finally, wc assume that when several chains compete, the total value of a 11 One must, also specify what happens if -zm occurs just after a fork starts, after a block 13,,, has just been solved. The probability of this event, is very small, and in practice it is not a very relevant, consideration, but, for completeness, wc need to specify the value of the reward earned by m(Bn) when K miners chain the block they curreni,ly

mine to while M -- K chain 13

+ 90 Time 53 Figure 4: Bitcoin price during the March 2013 fork. The graph plots individual transaction prices obtained from a major bitcoin exchange platform, Bitstamp, during the March 11-12, 2013 fork. The first dotted vertical line represents the time at which the fork started, and the second dotted vertical line represents the time at which the original chain caught up the fork. assume that at each time T e T, the realisation of a sunspot random variable rT is observed by all, and we include it in the state. r T is uniformly distributed on [0, 1] and i.i.d. over time. Thus, we define -- ( CT , AT , TT ) and denote by O the set of states of the world. Strategies: Miner m chooses his strategy to maximise his expected payoff at time zm. At each time T G T, miners observe the whole history of the game, that is, the state wr, as well as, e.g., the exact timing of blocks resolution and the previous mining choices. In the spirit of Markov perfection, 15 of them is hit by the liquidity shock. This is the case if a,ll miners stick to the original chain at any time T G T . If they do so the longest, chain rule (LCR) trivially holds. Our first, proposition states that there exists an equilibrium in which miners follow this strategy. Proposition 1 There exists a Markov Perfect Equilibrium in which, on the equilibrium path there is a single chain and all miners follow the LCR, thus obtaining their maximum expected payoff, The intuition for Proposition 1 is the following. When all miners up to T attach their blocks to the original chain, thus following the LCR, there is a, single chain at, T. If [he others abide (,his strategy, then m can obtain his maximum possible expected payoff, by a,lso abiding to it. Hence there is no profitable one shot deviation from the stra,tcgy which consists in extending the original (and thereby longest,) chain. Precisely, each miner rationally anticipates that if he deviates and solves a, block, the other miners would not; follow him, ancl the block solved out, of the equilibrium path would have no value. In the context, of the strategic interaction characteriscd in Proposition 1, miners are not, really compeling to solve their block before the others. That another miner solves his block before m cloes not, in itself, reduce m,'s gains. The only thing that matters for miners to obt,a,in the maximum payoff they get, in Proposition 1 is that, they coordinate well and all work on the same chain. It is also noteworthy that the result in Proposition 1 docs not depend on the number of miners M. The economic mecha,nism involvecl in Proposition 1 docs not hinge on strategic behaviour. It is purely driven by coordination effects, which would also be at, play in a competitive environment. Proposition 1 emphasiscs that; attaching blocks to the original chain is a simple way for miners to coorclinate their actions, and results in a single chain with no fork. There might, however, bc other ways for miners to coordinate in our stochastic game. In particular they could rely on the sunspot variable r T . Wc now exhibit an equilibrium in which conditioning actions on rr T leads Lo equilibria with forks. 54 Intuitively, suppose miners follow the original chain until the realisation of the sunspot, variable is such that, miners anticipate a fork. As shown below, because of coordination effects, this a,nticipation is self fulfilling. 17 "Gavin Andresen: the 0.8 fork is longer, yes? so majority hashpower is 0.8 . first rule of bitcoin: majority hashpower wins Luke Dashjr: if we go with 0.8 we are hard forking BTC Guild: I can single handedly put 0.7 back to the majority hashpower. I just need confirmation that that's what should be done. Pieter Wuille: that is what should be done, but we should have consensus first As illustrated by the above quoted discussions, miners faced a dilemma. Should they follow the longest chain rule and continue mining the 0.8 chain which had attracted the majority of the computing power? Or should they fork from it, reverting to a different version of the blockchain? The above discussion shows that the overarching concern of the miners was that they wanted to follow the consensus. BTC Guild, which was one of the largest pools at the time, eventually chose to downgrade to the 0.7 version. This resulted in the 0.7 chain becoming the longest, and all miners coordinating back to it. Consequently more than 24 blocks, solved on the 0.8 chain, became orphaned, and their miners (including BTC Guild) lost the corresponding rewards. Commenting on this situation, Narayanan (2015) wrote: "One way to look at this is that BTC Guild sacrificed revenues for the good of the network. But these actions can also be justified from a revenue-maximising perspective. If the BTC Guild operator believed that the 0.7 branch would win anyway (perhaps the developers would be able to convince another large pool operator), then moving first is relatively best, since delaying would only take BTC Guild further down the doomed branch.' This illustrates the behaviour of miners in Proposition 2: if one miner expects all the others to fork, then he is better off following them. Similarly to the 0.7 chain in the 2013 Bitcoin fork, in Proposition 2, the fork stemming from Bn(T) f becomes the only active chain. Since it does not include blocks

to Bn(T), 19 In our model miners hold their rewards until zm and therefore have vested interests. In practice, miners cannot sell their rewards immediately after solving blocks, due to the k-blocks rule. Our model takes a simplified view of this situation by assuming that the vesting period lasts until zm. Our next result illustrates the consequences of vested interests. To state that result, rank the miners by their vested interest in the original chain at time T f as follows

TO(m, where Pr(zm T') is the probability that at the next stopping time T', miner m is hit by a liquidity shock, and -- Nm(Tf ) = 1) is the probability that he

solves his block at T/. Condition 1 For any M and any K < M, G(K) + - K) = G(M), and WT is such that there exists K e {Int(}) + 2, ...M} (where Int denotes the integer part) such that

2 (1) 55 and for m > K

< v 0 (m, (2) while for m K

The assumption that for any M and any K < M, G(K) + G(M -- K) -- G(M), simplifies the presentation of Condition 1. However, Proposition 3 below also holds in the more general case where G(K)+G(M--K) G(M) . 56Consider an arbitrary integer f. Let Tf be the first time at which rT > 1 -- E, f < n(T) and Condition 1 holds. 21 of Proposition 3.

Original chain with M -- K miners New chain with K miners t 56 In addition to notational changes, it would require imposing an (arbitrarily large) upper bound on miners' vested interests. 56 Figure 5: Equilibrium of Proposition 3 Unlike Proposition 1 and Proposition 2, the conditions in Proposition 3 depend on the number of miners. More precisely, the tradeoffs faced by the miners involve the effect of their mining strategy on the value of their rewards. If miners were competitive and their choice had no impact on the value of their rewards, this strategic effect would not arise. Finally note that the equilibrium outcome in Proposition 3 is Pareto dominated by that in Proposition 1. Again, forking reduces the total gains of the miners, and yet it can arise in equilibrium.

Our analysis suggests that mining in a blockchain is a coordination game. Coordination games usually have multiple equilibria, some of which are Pareto dominated. Our first results illustrate that this can be the case in the blockchain, and raise an important point in the policy debate on blockchains: when record keeping is decentralised, efficient decentralisation requires coordination, while coordination problems can lead to inefficient equilibria. It would be interesting to study if 57 Intuitively, if difficulty was kept, constant, an increase in computing capacity would lead to an increase in the frequency of blocks validations. Instead of one block every 10 minutes, there could be, for example, one block every 8 minutes. The increase in difficulty would bring the average duration between two blocks back to minutes. 57 and how inefficient equilibria could be avoided. Maybe cheap talk could play a role in this context. This might provide a rationale for communication channels among miners and developers, such as IRC channels and forums. Another communication device used in practice by miners is flags attached to blocks to convey messages to other miners, such as, e.g., support for an upgrade, which might then lead to or help avoid a fork. It would also be interesting to identify the main drivers of blockchain instability. For example, one could analyse if concentration of computing power can be dangerous. One could also study if other reward schemes than that currently used in blockchains could generate better outcomes. For example, while Bit,coin does not reward orphaned blocks, Ethereum does, to some extent. Should onc expect, the latter reward scheme to generate better outcomes than the former? 25 Appendix Throughout the proofs we will use the following lemma: Lemma 1 Our blockchain game is continuous at infinity. Proof of Lemma 1: Denote by J(om) the expected payoff of miner m if he follows strategy cm. Consider an alternative strategy, am,i that prescribes the same actions as am until time T and differs afterwards. The difference between the two expected payoffs can be written as

Pr(zm < Now, by definition,

Moreover lim Pr(zm > T) 0, T+00 and J (0m) -- J(dm) is bounded, since is finite. Hence, lim J(om) -- J(dm) 0, 00 which ensures that our game is continuous at infinity. |

|